Life is full of investment decisions. Each one, whether big or small, will require some sort of financial capital – and naturally also necessitate one’s energy and commitment. Also, investments normally require an opportunity cost – the benefits that are forgone in choosing one option over other alternatives.

For these reasons and more, deciding on which investments to make may slip down the rings of one’s priority ladder (if they haven’t already). Knowing the effects of timing on investment strategies can help shape strategies that will be beneficial when retirement arrives.

In this Pinnacle Perspective, we evaluate the results you can expect when beginning your investment strategy at different times.

It is true – starting your investment strategy earlier in life may be the most widespread piece of advice financial professionals give. Starting earlier and consistently contributing to investment accounts has the advantage of allowing one to ride the ups and downs of the market, knowing that the long-term nature of the investment means the probability of making a return is high.

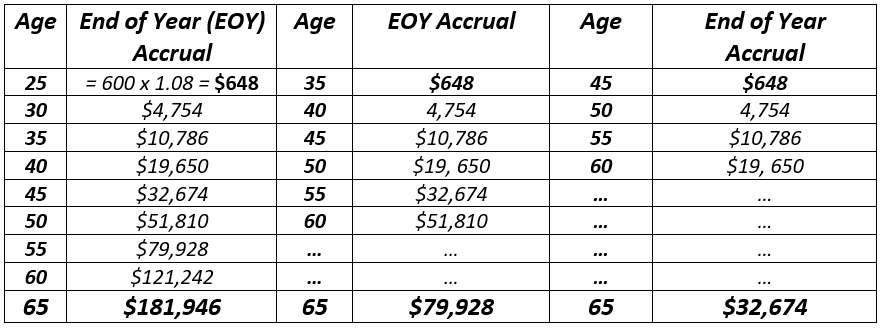

Below is a chart comparing the scenarios of beginning an investment strategy at different ages. Each scenario assumes a retirement age of 65, an 8% annual return, and a contribution of $50 a month ($600/year).

Someone who begins this investment strategy at 25 will see their contributions culminate in $181,946 when they retire. Applying this same scenario to someone who began at age 35, their 30 years of investment would accumulate to $79,928 – less than half. And for someone who begins at 45, the amount reduces to $32,674.

As the saying goes, “Slow and steady wins the race.”

It is important to note that an 8% percent return is not guaranteed. Market fluctuations may mean returns can be exciting or concerning. Similarly, these figures need to be viewed with the lens that taxes and inflation will affect your purchasing power – that is, the value of your money today will not look the same in 30 years.

On the other side, there are advantages to beginning an investment strategy at 40.

For one, an individual probably rakes in a higher income. As one enters their forties, the likelihood of being able to start off their investments at a higher amount and continually contribute is higher as opposed to the beginning of your career.

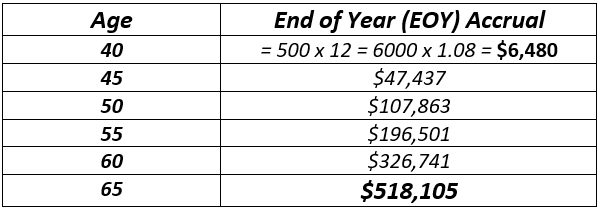

The following chart depicts the money accrued if one began an investment strategy at 40 andcontributed $500/MO with a consistent 8% return.

Starting later with an increased contribution raked in over half a million dollars. Again, an 8% return is not guaranteed. However, the math does drive in the point – there is never a bad time to choose to grow one’s money.

Another advantage of starting an investment strategy later in life would be that one’s human capital is likely to have grown and accumulated traction. Human capital can be defined as “the collective skills, knowledge, or other intangible assets of individuals that can be used to create economic value for the individuals, their employers, or their community.” Albeit an intangible and less calculated form of wealth, it is an aspect that cannot be overlooked. As one’s skills, experience, network of relationships, etc. grow, the probability of that translating into increased income also grows.

We encourage you to evaluate your investment strategy – smart money management is available at any age. Regardless of whether your investment strategy begins in your 20s or 40s, there are pathways you can follow to reach your personal financial goals. Schedule an appointment with one of our advisors and see how you can prepare for the years to come.