As of this writing, Jeff Bezos – founder of Amazon – is the world’s wealthiest person, with a net worth close to $192B.

As of March 2021, the U.S. national debt exceeded $28 trillion.

That means the world’s largest fortune is 1/146th the size of our national debt.

“If our government wants to keep the lights on, then it is going to need more income, which not only means that you can count on being taxed, but also on being taxed at an increasing rate.”

– Source: THE FUTURE OF US TAXATION: And how to prepare. By NICK STOVALL, CPA/PFSSM, MBA

What’s The BIG Deal?

From a historical point of view, marginal tax rates are relatively low. The last time the U.S. national debt was even close to the same percentage of GDP as it is today was at the end of World War II. The maximum marginal tax rate at that time was about 90%, while today it is 37%. The high post-war tax revenue helped the country dig out of a deep hole, while today’s tax revenue does not even cover our annual budget—much less our cumulative national debt.

In addition, our unfunded liabilities have only increased through the years. These liabilities exist outside of the annual budgetary debt discussed above and are due to programs such as Social Security, Medicare and government pensions. Why these unfunded liabilities are so concerningis thatwe are just in the beginning phase of the greatest retirement wave in U.S. history, and these new retirees are quickly depleting the thin reserves of Medicare and Social Security.

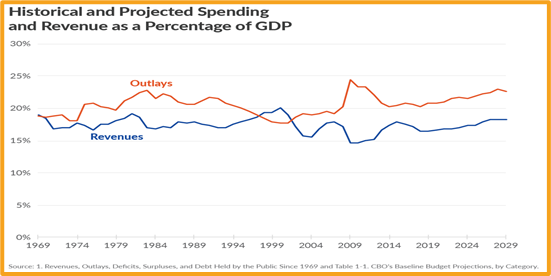

To put unfunded liabilities into perspective, consider these as off-balance-sheet obligations similar to those that bankrupted Enron*. Although these are not listed as part of the national debt, they must be paid just the same. The difference between the Enron debacle and U.S. unfunded liabilities is that the U.S. government has the legal authority to raise taxes and print more money—both of which could have long-term negative consequences. Of course, the government also has the authority to reduce expenses and operate under a balanced budget, but since the late 1990s neither political party has proven to have the courage and discipline to use that authority. Therefore, the most likely scenario is a future of higher taxes and increased inflation, especially when considering the continued deficit spending as projected by the Congressional Budget Office:

What Can I Do About It?

“It is easier to make more money by saving on taxes than by just making more money.”

– Source: THE FUTURE OF US TAXATION: And how to prepare. By NICK STOVALL, CPA/PFSSM, MBA

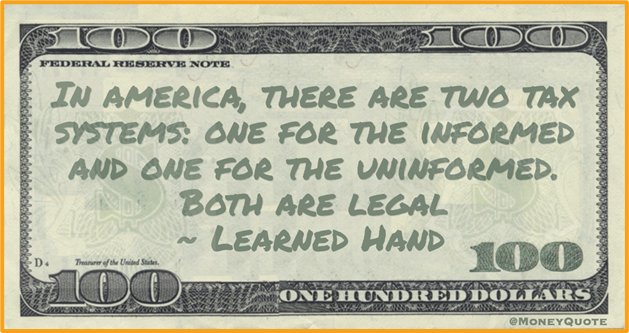

That statement is not always true, but the idea could be valuable to people who are approaching or who are in retirement. As simple as it sounds, it is difficult to achieve without a comprehensive and coordinated income plan. Most people we meet have spent most of their adult lives focused on accumulating wealth in a tax-deferred manner, with an eye toward retirement, but very little time developing a plan for properly distributing their wealth tax-efficiently during retirement and at their death. Therefore, we help our clients develop a coordinated retirement income and legacy plan that starts with comparing a specific income need against all income sources, such as earned income, pensions, Social Security, investment real estate, stock dividends, interest-bearing assets, life insurance withdrawals/ loans, annuities and traditional/Roth IRA distributions. However, as part of the plan, we also answer the question “Which income sources should I take, and when, to minimize my tax burden?” because our experience has been that most of our clients are unfamiliar with the two tax systems in the U.S. as explained by Judge Learned Hand:

Should I Diversify My Tax Burden?

Yes! Despite the future tax risks that exist, the reality is that no one knows if or when those changes will occur, or how much the change will be. Our opinion and advice for most people is that the foundation of a tax portfolio should be tax-free money, while still diversifying with “free money”, tax-deferred money and taxable money. Here are some examples of the four areas of tax diversification:

Free Money:

- Employer Match to Employer Plan

Tax-Free Money:

- Roth IRA

- Life Insurance

- Municipal Bonds

Tax-Deferred Money:

- Traditional IRA

- Employer Plan

- Non-Qualified Annuity

Taxable Money:

- Ordinary Income

- Capital Gains & Dividends

What Are The Best Conversion Options?

If you believe there is a risk of taxes going up in the future, then the important question is “Do you want to pay tax on your seed or on your harvest?” If your answer is to “pay tax on your seed”, and you have accumulated significant tax-deferred retirement accounts, then choosing one or more of the three conversion strategies may be appropriate. Like most things in life, there are pros and cons to each strategy, and the choice to implement one or more of the strategies would depend heavily on the unique age, goals, portfolio size, opinions, family situation, and income sources situation of each person. Before implementing any tax conversion strategy, considerations need to be made such as:

- How much can be converted each year without going into a “high” tax bracket or triggering unintended consequences like Medicare surcharges, Social Security taxation, or capital gains taxation?

- What time period is there to convert before the expiration of certain tax-reduction provisions?

- Which funds should be used to pay the conversion tax?

With that in mind, here are summaries of the

three most popular tax conversion strategies that we help our clients implement:

- Traditional IRA to Roth IRA Conversion Strategy – This strategy is the most popular and could make sense for most people worried about future tax increases. The result of this strategy is that the Roth account would grow tax free, could be distributed tax free during retirement and would transfer to heirs income tax free at death.

- Traditional IRA to Real Estate Conversion Strategy – Some of our clients desire passive income from rental properties. The result of this conversion strategy is the real estate would grow tax deferred, could cash flow tax efficiently during retirement (via depreciation), could be exchanged tax free (via 1031 exchange) and would transfer to heirs income tax free at death (via “step up in basis”). As of March 2021, there is political sentiment and discussions to remove the “step up in basis” at death, which would cause gains to be taxable to heirs.

- Traditional IRA to Life Insurance Conversion Strategy – Some of our clients desire market-based returns with no market risk, and/or desire other living benefits such as long term care benefits, or a death benefit for legacy planning. The result of this conversion strategy is that the account would grow tax deferred, could be distributed tax free during retirement, and would transfer to heirs income tax free at death.

Any Last Thoughts?

All else being equal, it would not matter if you put your money into a taxable, tax‐deferred, or tax‐free account as long as income tax rates never change (in other words, the mathematical net amount you receive in the end will be the same). Unfortunately, tax rates have changed and will change over time; thus, there is a strong incentive to operate in the “tax system of the informed” (as Judge Learned Hand encouraged us).

Regardless of where you are saving for retirement, the fact you are saving anywhere is a good thing!

Keep it up, but try to retain as many of those dollars in your pocket as possible by avoiding the retirement landmine of tax risk.

We look forward to helping you have a safer and more enjoyable journey. To schedule an appointment to talk in-depth about the best tax strategies for your financial well-being, click here. You can also reach out to us via phone at (719) 722-2992.